Discrete Random Variables

Binomial Random Variable:

Here’s what we know:

- we have n independent trials

- we have two possible outcomes

- the probability of success is p (same for every trial)

- this makes the probability of failure as (1-p)

if X represents the number of successes that occur in the n trials, then X is a binomial random variable with parameters (n,p).

\[P(X = x) = {n \choose x} p^x (1-p)^{n-x}\] \[\text{where } {n \choose p} = \frac{n!}{p!n-p!}\]Example: It’s known that any item produced by a certain machine will be defective with probability 0.1 (independent of any other item). What is the probability that in a sample of three items, at most one will be defective?

With X as the number of defective items in the same, then X is a bionomial random variable with parameters n = 3 and p = 0.1.

We want to know the probability that at most one will be defective, that is. We want to know the summation of $P($none are defective$)$ + $P($one is defective$)$ = $P(X=0) + P(X=1)$

\[= {3 \choose 0}(0.1)^0(0.9)^3 + {3 \choose 1}(0.1)^1(0.9)^2 = 0.972\]import numpy as np

import math

import matplotlib.pyplot as plt

def binomial(n, p, x):

return math.comb(n, x) * (p**x) * (1-p)**(n-x)

print(binomial(3, 0.1, 0) + binomial(3, 0.1, 1))

0.9720000000000002

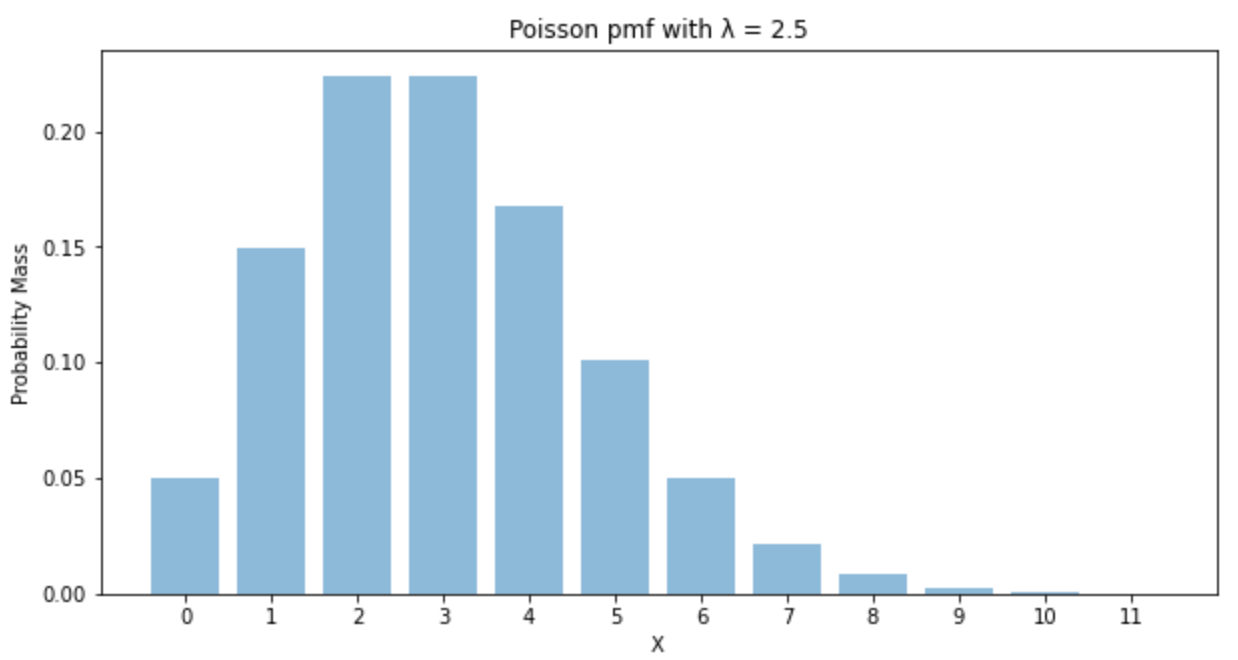

Poisson Random Variable

Here’s what we know:

- Poisson distribution describes the number of events that occur within a given time interval

- Poisson is a discrete distribution, meaning the events mentioned above must be discrete and cannot be continuous (i.e. “number of purchases” and “number of people entering a bank” are both discrete)

- $\lambda$ represents the expected number of events per time interval

- it is bounded by $0$ and $\infty$. *

Some underlying assumptions for us to remember:

- the rate at which the events occur is constant

- events are independent, meaning the occurrence of one event happening does not impact others from happening

Probability Mass Function (pmf):

the probability (height) of getting each of these discrete outcomes is modeled by:

\[P(X = x) = e^{-\lambda} \frac{\lambda^x}{x!}, \text{ for } x \geq 0\]Below is a plot to get a better understanding:

import numpy as np

import math

import matplotlib.pyplot as plt

def poisson_pdf(lam, x):

return (np.exp(-lam)*lam**x)/(math.factorial(x))

def plot_pmf(lam):

y_axis = np.array([poisson_pdf(3, x) for x in range(0,int(lam*5))])

x_axis = [x for x in range(0,int(lam*5))]

plt.figure(figsize=(10,5))

plt.bar(x_axis, y_axis, align='center', alpha=0.5)

plt.xticks(x_axis)

plt.ylabel('Probability Mass')

plt.xlabel('X')

plt.title('Poisson pmf with λ = {}'.format(lam))

plt.show();

return

plot_pmf(2.5)